You've probably noticed that the same grocery run costs more than it did a few years ago. A coffee that used to be $3 is now $4.50. A tank of gas stretches your budget further than it once did. This is inflation at work, and understanding how it operates can help you make smarter financial and business decisions.

This post breaks down what inflation actually means, what causes it, how it's tracked, and what it means for your wallet and your business.

What Is Inflation?

Inflation is the rate at which prices rise over a given period, typically measured year over year. According to the International Monetary Fund (IMF), inflation represents "how much more expensive the relevant set of goods and/or services has become over a certain period."

Put simply: if a basket of groceries cost $100 last year and costs $104 this year, the inflation rate for that basket is 4%.

The flip side of rising prices is falling purchasing power. Purchasing power refers to how much you can actually buy with a given amount of money. When prices go up, each dollar you hold buys a little less than it did before. For people on fixed incomes or those whose wages aren't keeping pace with price increases, this erosion of purchasing power is the most direct and painful effect of inflation.

Is Inflation Good or Bad?

The honest answer is: it depends on how much there is.

Most economists agree that low, stable, and predictable inflation is actually healthy for an economy. The U.S. Federal Reserve targets an annual inflation rate of around 2%. At that level, prices rise gradually enough that consumers are encouraged to spend now rather than wait, which keeps economic activity moving.

The problems start when inflation gets too high. High inflation makes it hard for people and businesses to plan ahead. It erodes savings, squeezes household budgets, and forces companies to constantly adjust their pricing. At the extreme end, you get hyperinflation, which is when inflation spirals completely out of control. Zimbabwe's 2008 hyperinflation crisis is one of the most well-known examples, with annual inflation estimated at 500 billion percent at its peak, according to the IMF. The national currency became virtually worthless, and the country ultimately abandoned it.

Deflation, or falling prices, sounds appealing but comes with its own problems. When consumers expect prices to keep dropping, they delay purchases. Less spending means less revenue for businesses, which leads to slower growth, job cuts, and economic stagnation. Japan spent much of the 1990s and 2000s trapped in deflationary stagnation, which economists still study today as a cautionary example.

What Causes Inflation?

Inflation rarely has a single cause. It usually results from a combination of forces:

Demand-pull inflation: This happens when demand for goods and services outpaces supply. More money chasing fewer goods pushes prices up. Government stimulus spending or a booming stock market can trigger this effect.

Cost-push inflation: When it becomes more expensive to produce goods, businesses pass those costs on to consumers. Sharp increases in oil prices, for example, can trigger cost-push inflation across many industries simultaneously.

Money supply growth: When the amount of money in circulation grows faster than the economy's output, each unit of currency loses value. This relationship is known as the quantity theory of money and is one of the oldest principles in economics.

Inflation expectations: If workers expect prices to rise, they demand higher wages. If businesses expect costs to climb, they raise prices preemptively. These expectations can become self-fulfilling, creating a cycle that's difficult to break.

How Does Inflation Affect Businesses?

Inflation hits businesses from multiple directions at once.

On the cost side, raw materials become more expensive, rent and utilities go up, and wages need to increase to keep pace with the cost of living. These pressures squeeze profit margins, especially for businesses that can't easily raise their own prices.

On the revenue side, there are some silver linings. Businesses with high existing inventory can sell it at higher prices than they originally anticipated, improving margins. Early-stage borrowing at fixed interest rates becomes cheaper over time as the real value of that debt falls.

Not all businesses feel inflation equally. Essential goods and services, like healthcare, food, and fuel, tend to hold their demand even as prices rise. Discretionary goods are far more vulnerable. If consumers need to cut back, luxury items and non-essentials are usually the first to go.

According to Oracle NetSuite, a survey by the National Federation of Independent Businesses (NFIB) in February 2022 found that 26% of small business owners named inflation as their single biggest problem, up from just 2% the prior year. That surge reflects how quickly inflation can shift from a background concern to a genuine operational crisis.

For businesses, the smartest responses to inflation include diversifying suppliers, locking in fixed-rate borrowing, and reviewing product portfolios to focus on higher-margin offerings.

How Is Inflation Measured?

The most widely used tool for tracking inflation is the Consumer Price Index (CPI), published in the U.S. by the Bureau of Labor Statistics (BLS). The CPI tracks the cost of a "basket" of goods and services that a typical urban household buys, including food, housing, transportation, and healthcare. By comparing the cost of that basket over time, economists can calculate how fast prices are changing.

Here's a simple example: a local bakery spends $1,000 per month on flour. After inflation, that cost rises to $1,200. If the bakery keeps its bread prices the same, profits shrink. To protect its margins, the bakery may raise prices, renegotiate with suppliers, or cut costs elsewhere.

The BLS also tracks "core inflation," which strips out volatile food and energy prices to give a clearer picture of underlying price trends. This is the figure that policymakers often pay closest attention to when setting interest rates.

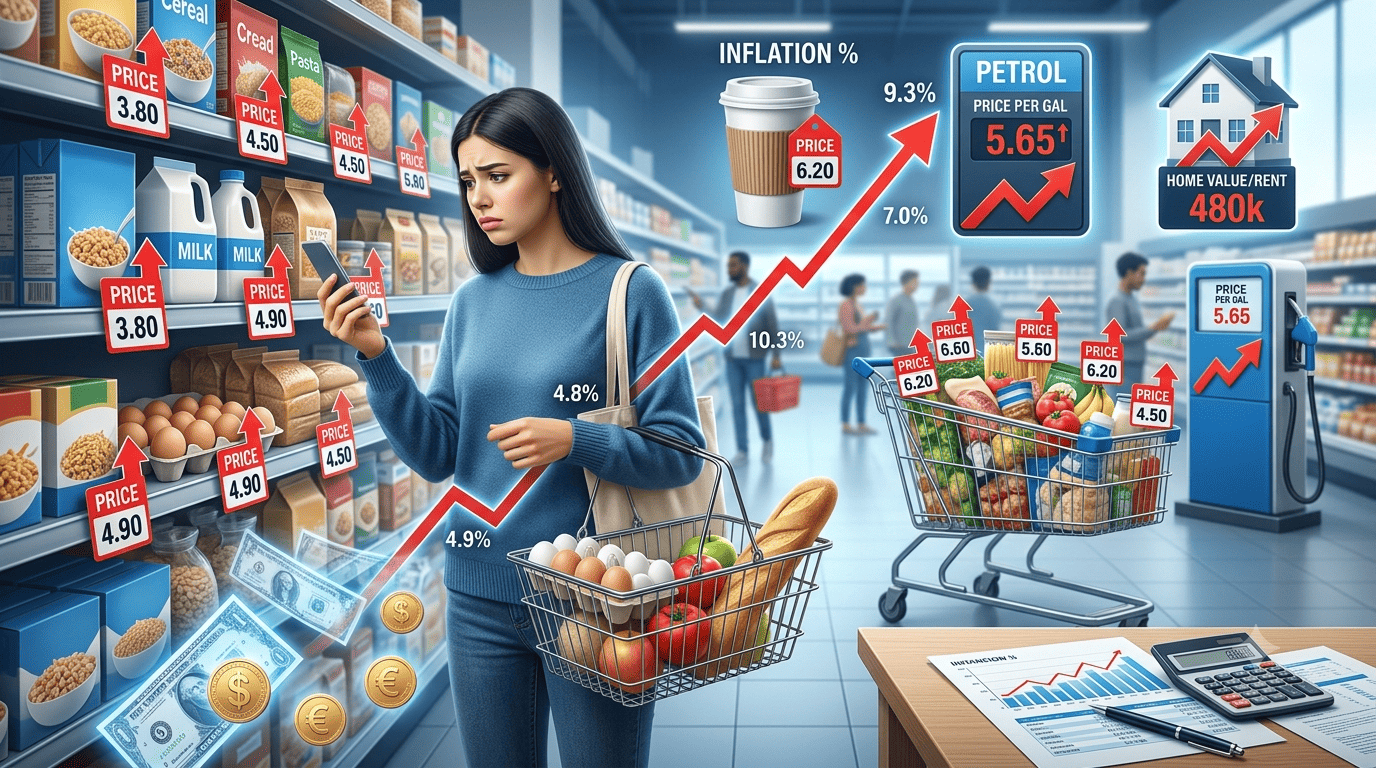

According to the BLS Consumer Price Index Summary released in June 2026, the CPI-U (Consumer Price Index for All Urban Consumers) increased 4.2% over the 12 months ending in May 2026. Energy prices were a major driver, with the energy index rising 23.5% over the same period and gasoline prices climbing 40.5%. Food prices rose 3.1% over the year.

These numbers matter because they directly affect how far your paycheck stretches and what businesses pay to operate.

How to Calculate the Inflation Rate Formula

Economists use a simple formula to calculate how much prices have changed over time: Inflation Rate (%) = ((Current CPI - Previous CPI) / Previous CPI) × 100. Here, the Current CPI is the Consumer Price Index value for the period you are measuring, while the Previous CPI is the value from an earlier period you are comparing it to. The result tells you the percentage by which prices have risen. A positive number means prices went up, so your money buys less than it did before. For example, if the CPI was 200 last year and is 210 this year, the inflation rate would be 5%, meaning the average cost of goods and services rose by 5% over that period.

The Current CPI is the Consumer Price Index value for the time period you are measuring right now. The Previous CPI is the value from an earlier period, such as the previous year, that you are comparing it to. When you plug these numbers into the formula, the result is a percentage. A positive percentage means prices have gone up, so your money buys less than it used to. A negative percentage means prices have fallen. The bigger the percentage, the faster prices are changing. For example, if the CPI was 200 last year and is 210 this year, the inflation rate is 5%, meaning the average cost of goods and services rose by 5% over that period.

How Can People Protect Themselves from Inflation?

Understanding inflation is only useful if you can act on it. Here are several practical steps individuals can take to protect their purchasing power:

Invest rather than hold cash: Money sitting in a low-interest savings account loses value during periods of high inflation. Investing in assets like index funds, real estate, or equities has historically provided returns that outpace inflation over the long term.

Consider inflation-protected securities: The U.S. Treasury offers Treasury Inflation-Protected Securities (TIPS) and Series I savings bonds (I-bonds), both of which are specifically designed to maintain purchasing power by adjusting with the inflation rate.

Negotiate your salary: If your income is not keeping pace with inflation, you're effectively taking a pay cut. Use inflation data to anchor salary conversations with your employer.

Review and adjust your budget: Periods of rising prices are a good time to audit your spending, cut non-essential costs, and redirect savings toward assets that hold their value.

Lock in fixed costs where possible: Fixed-rate mortgages and long-term rental agreements can shield you from future price increases in housing.

Key Takeaways

Inflation measures the rate at which prices rise over time, which directly reduces purchasing power.

Low, stable inflation (around 2%) is generally healthy. High or unpredictable inflation causes economic harm.

The main causes are excess demand, supply disruptions, excess money supply, and inflation expectations.

Businesses face rising costs, margin pressure, and behavioral shifts in consumer spending during inflationary periods.

The CPI is the standard tool used to measure inflation. In the U.S., it rose 4.2% year-over-year as of May 2026, according to the BLS.

Individuals can protect their purchasing power through smart investing, inflation-linked securities, salary negotiation, and fixed-rate borrowing.

Build a Stronger Financial Foundation

Inflation is one of those forces that works quietly in the background until it suddenly becomes impossible to ignore. The more clearly you understand how it works, the better positioned you are to make decisions that protect your finances, your business, and your long-term goals.

Start by reviewing where your money sits. Is it working as hard as it could? Are your savings losing value in real terms? These are the questions that separate people who get ahead of inflation from those who feel its effects without understanding why.