Quick answer: Memory chip prices 2026 are surging as chip makers shift production toward artificial intelligence data centers and away from consumer devices. DRAM prices have jumped 171% in a single year. The result is higher prices for phones, laptops, and gaming consoles through 2027 and beyond.

For decades, the rule was simple. Memory got cheaper every year. You paid less and got more. A generation of buyers and businesses came to expect it.

That era is over.

The cost of building a phone or laptop is climbing fast, and the reason has little to do with the devices themselves. It comes down to one force reshaping the entire technology supply chain: the global race to build artificial intelligence. This post breaks down what is driving the memory price crisis, why it is a long-term shift rather than a short-term spike, and what it means for anyone who buys, builds, or sells technology.

Three Business Terms Worth Knowing First

Before we go deeper, here are three terms that explain the whole story:

DRAM (Dynamic Random Access Memory): the standard memory, or RAM, inside nearly every phone, laptop, and server.

HBM (High Bandwidth Memory): a premium chip built for AI that earns far higher profit than standard DRAM.

Hyperscalers: the giant cloud companies building AI data centers, including Microsoft, Google, Amazon, and Meta.

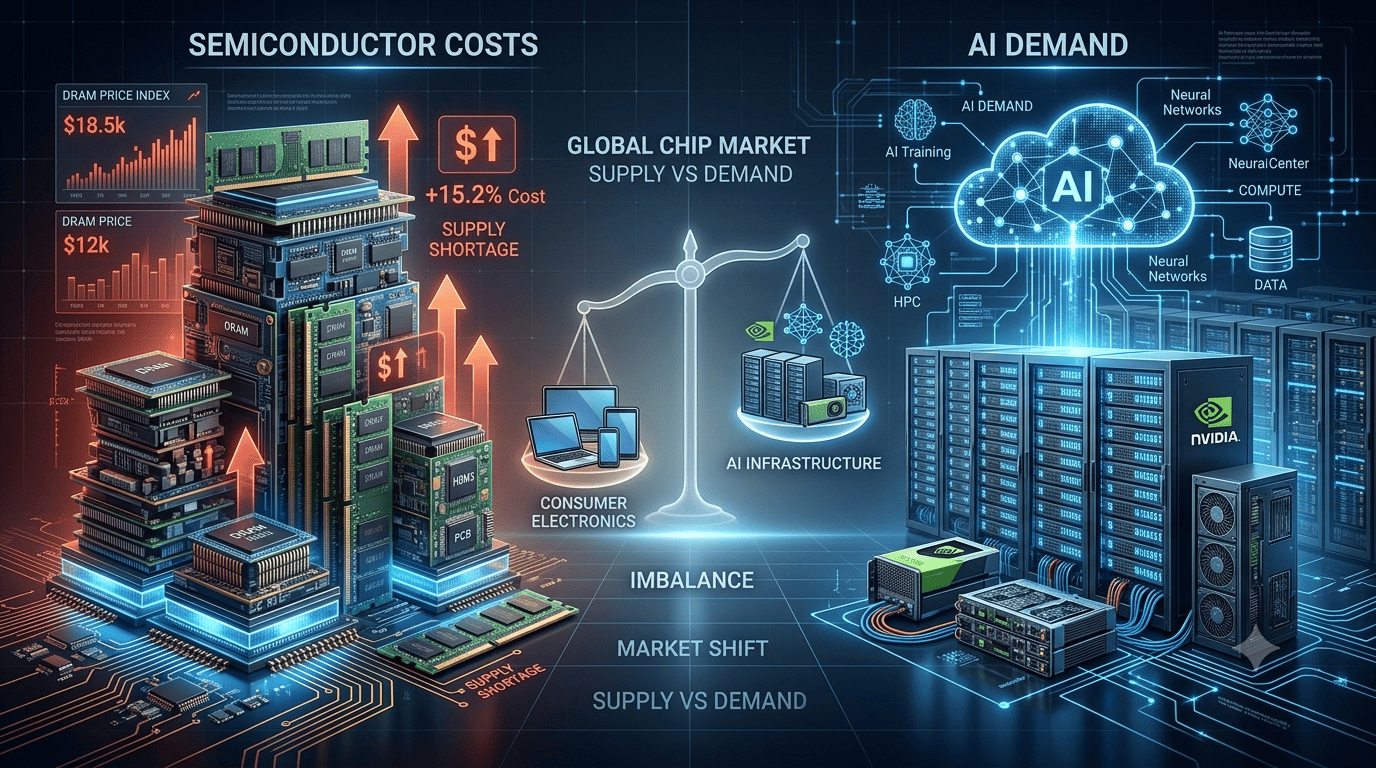

Memory Chip Prices 2026: What Is Actually Happening?

The numbers tell a clear story. According to the Bloomsbury Intelligence and Security Institute, DRAM prices have risen 171% year on year. DDR5 spot prices have quadrupled since September 2025.

And the trend is not slowing. Counterpoint Research estimates memory prices will jump another 40% to 50% in the first quarter of 2026, after last year's 50% surge. Semiconductor distributor Fusion Worldwide reports something even more striking: "Over the last two quarters, we've seen 1,000% price inflation in some products."

One real example makes it concrete. A Kingston 64GB DDR5 memory kit sold for $229.99 in October 2025. By December, the same kit cost $629.99, nearly triple, in two months.

Device makers are responding the only way they can. Dell, Lenovo, HP, Acer, and ASUS have all confirmed price increases of 15% to 20%. Memory now accounts for between 15% and 40% of a device's total production cost, depending on the product. This is not a temporary blip. It is a full reset.

Why Is AI Pulling Memory Away From Consumer Devices?

The core reason is simple economics. HBM earns several times the profit of standard DRAM, so factory owners point their capacity toward the chips that pay more. Two forces make this a lasting shift.

First, scale. AI servers need roughly six times more memory than standard servers. As hyperscalers build larger AI clusters, their demand has outgrown what suppliers can produce. Data centers are expected to consume up to 70% of all high-end memory in 2026.

Second, factory space. Each gigabyte of HBM uses about three times more factory capacity than standard DDR5. When production shifts to HBM, the supply of everyday memory drops, even though factories are running at full speed. As IDC put it, "every wafer allocated to an HBM stack for an Nvidia GPU is a wafer denied to the LPDDR5X module of a mid-range smartphone."

The money behind this is enormous. Major technology companies are expected to invest roughly $600 billion in AI infrastructure in 2026, a 36% jump in a single year. That spending gives hyperscalers extraordinary control over global memory supply.

How Does This Affect Costs, Margins, and Consumers?

The business impact arrives in three forms:

Higher input costs. Memory is now a major cost item in every device and server, flowing directly into production budgets.

Squeezed margins. Companies must either raise prices and risk losing customers, or absorb the cost and watch profits fall.

Supply risk. Getting enough memory is now a real problem, not just a pricing one. Intel CEO Lip-Bu Tan noted that smaller firms "are missing the memory, they cannot complete the products."

For consumers, this means three things: higher prices, weaker specifications for the same budget, and longer gaps between upgrades. Some smartphone makers are already cutting memory in new models to hold prices steady. IDC forecasts the PC market could shrink by up to 8.9% in 2026, while the smartphone market could fall by as much as 5.2%.

How Are Companies Responding to the Shortage?

Responses fall into two groups: those protecting their supply, and those passing on the pain.

The largest players have the advantage. Apple and Samsung lock in memory supply 12 to 24 months in advance through long-term contracts. As Morningstar analyst William Kerwin explained, "Apple is better-positioned, as it uses contract pricing rather than more volatile spot pricing." Smaller brands enjoy no such protection.

Pricing moves are already visible across the market:

Apple raised prices on MacBooks and iPads by up to 20%.

Xbox increased console prices by as much as $150 in a single update cycle.

Micron exited the consumer memory business through its Crucial brand, redirecting supply toward AI demand.

Some chip suppliers have paused price quotes entirely, expecting further increases.

On the production side, the big bets are being placed. Micron has committed $200 billion to US manufacturing. Samsung plans to grow its HBM capacity by 50% in 2026. But new factories take years to open. Relief is still a long way off.

What Could Happen Next? Three Scenarios Through 2027

Best case. Memory production expands faster than expected, AI demand stabilizes, and price increases slow in late 2026.

Base case. Prices continue rising moderately through 2026 and 2027 as suppliers keep prioritizing high-margin AI chips. Supply rebalances only gradually.

Worst case. AI demand keeps accelerating while new capacity arrives too slowly. The shortage deepens, pushing further sharp price hikes across phones, PCs, and consoles.

Most analysts expect the base case. The financial incentives for memory makers have not changed, and semiconductor plants take two to three years to reach full production.

The Key Insights for Business Learners

This crisis offers lessons that reach far beyond memory chips:

One component can move an entire market. A shortage in RAM is now reshaping pricing across phones, laptops, cloud services, and gaming.

Strategic allocation reshapes competition. When suppliers choose AI buyers over consumer makers, the balance of power shifts overnight. SK Hynix recently overtook Samsung in DRAM revenue for the first time since 1992.

Cost pressure flows to the customer. When margins are thin, companies pass increases along. Premiumization (focusing on higher-priced, higher-margin products) becomes the common response.

Affordability now depends on global decisions. The price of your next laptop is tied to how three companies, which control 95% of global supply, choose to allocate their factories.

Plan Now, Not After the Next Price Hike

Memory has gone from a cheap, predictable cost to a strategic resource. The old assumption (that memory would always get cheaper) no longer holds.

The takeaway is clear. Rising memory chip costs show how AI infrastructure demand is now shaping the price of everyday technology, pushing the industry from an era of low-cost expansion into one of sustained cost pressure. For students and future business leaders, this is a live case study in how a single shift in supply strategy can ripple across an entire global market.

Watch this trend closely. It is far from over.